Nuclear Power in Crisis: We Are Entering the Era of Nuclear Decommissioning

Nuclear power is in crisis ‒ as even the most strident nuclear enthusiasts acknowledge ‒ and it is likely that a new era is fast emerging, writes Jim Green, editor of the Nuclear Monitor newsletter. After a growth spurt from the 1960s to the ’90s, then 20 years of stagnation, the Era of Nuclear Decommissioning is upon us. Article courtesy Nuclear Monitor.

Last year was supposed to be a good year for nuclear power ‒ the peak of a mini-renaissance resulting from a large number of reactor construction starts in the three years before the Fukushima disaster. The World Nuclear Association (WNA) anticipated 19 reactor grid connections (start-ups) in 2017 but in fact there were only four start-ups (Chasnupp-4 in Pakistan; Fuqing-4, Yangjiang-4 and Tianwan-3 in China).

The four start-ups were outnumbered by five permanent shut-downs (Kori-1 in South Korea; Oskashamn-1 in Sweden; Gundremmingen-B in Germany; Ohi 1 and 2 in Japan).

The WNA’s estimate for reactor start-ups in 2017 was hopelessly wrong but, for what it’s worth, here are the Association’s projections for start-ups in the coming years:

2018‒19: 30

2020‒21: 12

2022‒23: 9

2024‒25: 2

Thus ‒ notwithstanding the low number of start-ups in 2017 ‒ the mini-renaissance that gathered steam in the three years before the Fukushima disaster probably has two or three years to run. Beyond that, it’s near-impossible to see start-ups outpacing closures.

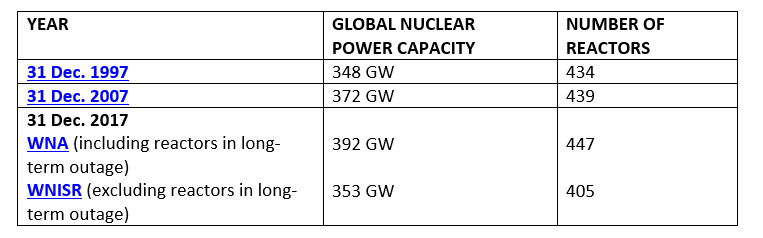

New nuclear capacity of 3.3 gigawatts (GW) in 2017 was outweighed by lost capacity of 4.6 GW. Over the past 20 years, there has been modest growth (12.6%, 44 GW) in global nuclear power capacity if reactors currently in long-term outage are included. However, including those reactors ‒ in particular idle reactors in Japan, many of which will never restart ‒ in the count of ‘operable’ or ‘operational’ or ‘operating’ reactors is, as former WNA executive Steve Kidd states, “misleading” and “clearly ridiculous”.

There would need to be an average of 10 reactor start-ups (10 GW) per year just to maintain current capacity. The industry will have to run hard just to stand still

The World Nuclear Industry Status Report (WNISR) excludes reactors in long-term outage ‒ defined as reactors that produced zero power in the previous calendar year and in the first half of the current calendar year ‒ from its count of operating reactors. Thirty-six reactors are currently in long-term outage, 31 of them in Japan.

Excluding reactors in long-term outage, the number of reactors has declined by 29 over the past 20 years, while capacity has grown by a negligible 1.4% (5 GW). Over the past decade, the reactor count is down by 34 and capacity is down by 9.5% (19 GW).

The industry faces severe problems, not least the ageing of the global reactor fleet. The average age of the reactor fleet continues to rise, and by mid-2017 stood at 29.3 years; over half have operated for 31 years or more.

The International Energy Agency expects a “wave of retirements of ageing nuclear reactors” and an “unprecedented rate of decommissioning” ‒ almost 200 reactor shut-downs between 2014 and 2040. The International Atomic Energy Agency anticipates 320 GW of retirements by 2050 ‒ in other words, there would need to be an average of 10 reactor start-ups (10 GW) per year just to maintain current capacity. The industry will have to run hard just to stand still.

Renewables (24.5% of global generation) generate more than twice as much electricity as nuclear power (<10.5%) and the gap is growing rapidly

Assuming the mini-renaissance doesn’t continue to flop (as it did in 2017), an average of 10 or so start-ups from 2015‒2020 is possible (there were 24 start-ups from 2015‒17). But to maintain that level, the number of construction starts would need to increase sharply and there is no likelihood of that eventuating ‒ there have only been seven construction starts in the past two years combined.

The number of reactors under construction is slowly dropping. Using WNA figures, 71 reactors were under construction in January 2014 compared to 58 in January 2018. According to WNISR figures, the number is down from 67 to 52 over the same period. That trend seems certain to continue because of a sharp drop in reactor construction starts: 38 from 2008‒2010 compared to 39 in the seven years from 2011‒2017.

Nuclear power accounted for 10.5% of global electricity generation in 2016 (presumably a little less now), well down from the historic peak of 17.5% in 1996.

Renewables (24.5% of global generation) generate more than twice as much electricity as nuclear power (<10.5%) and the gap is growing rapidly. The International Energy Agency predicts renewable energy capacity growth of 43% (920 GW) from 2017 to 2022. Overall, the share of renewables in power generation will reach 30% in 2022 according to the IEA. By then, nuclear’s share will be around 10% and renewables will be out-generating nuclear by a factor of three.

A disastrous year for the nuclear industry

Last year was “all in all a disastrous year” for the nuclear power industry according to Energy Post Weekly editor Karel Beckman. Nuclear lobbyists issued any number of warnings about nuclear power’s “rapidly accelerating crisis“, a “crisis that threatens the death of nuclear energy in the West“, “the crisis that the nuclear industry is presently facing in developed countries“, the “ashes of today’s dying industry”, and noting that “the industry is on life support in the United States and other developed economies“.

Lobbyists engaged each other in heated arguments over possible solutions to nuclear power’s crisis ‒ in a nutshell, some favour industry consolidation while others think innovation is essential, all of them think that taxpayer subsidies need to be massively increased, and none of them are interested in the tedious work of building public support by strengthening nuclear safety and regulatory standards, strengthening the safeguards system, etc.

One indication of the industry’s desperation has been the recent willingness of industry bodies (such as the US Nuclear Energy Institute) and supporters (such as former US energy secretary Ernest Moniz) to openly acknowledge the connections between nuclear power and weapons, and using those connections as an argument for increased taxpayer subsidies for nuclear power and the broader ‘civil’ nuclear fuel cycle. The power/weapons connections are also evident with Saudi Arabia’s plan to introduce nuclear power and the regime’s pursuit of a weapons capability.

There were no commercial reactor construction starts in China in 2017 (though work began on one demonstration fast neutron reactor) and only two in 2016

The biggest disaster for the nuclear industry in 2017 was the bankruptcy filing of Westinghouse ‒ which also came close to bankrupting its parent company Toshiba ‒ and the decision to abandontwo partially-built reactors in South Carolina after the expenditure of at least US$9 billion. As of January 2018, both Westinghouse and Toshiba are still undergoing slow and painful restructuring processes, and both companies are firmly committed to exiting the reactor construction business (but not the nuclear industry altogether).

Another alarming development for the nuclear industry was the slow-down in China. China Nuclear Engineering Corp, the country’s leading nuclear construction firm, noted in early 2017 that the “Chinese nuclear industry has stepped into a declining cycle” because the “State Council approved very few new-build projects in the past years”.

There were no commercial reactor construction starts in China in 2017 (though work began on one demonstration fast neutron reactor) and only two in 2016. The pace will pick up but it seems less and less likely that growth in China will make up for the decline in the rest of the world.

The Era of Nuclear Decommissioning will be characterised by escalating battles (and escalating sticker shock) over lifespan extensions, decommissioning and nuclear waste management

The legislated plan to reduce France’s reliance on nuclear from 75% of electricity generation to 50% by 2025 seems unlikely to be realised but the government is resolved to steadily reduce reliance on nuclear in favour of renewables. French environment minister Nicolas Hulot saidin November 2017 that the 50% figure will be reached between 2030 and 2035. France’s nuclear industry is in its “worst situation ever”, a former EDF director said in November 2016, and the situation has worsened since then.

There were plenty of other serious problems for nuclear power around the world in 2017:

- Swiss voters supported a nuclear phase-out referendum.

- South Korea’s new government will halt plans to build new nuclear power plants (though construction of two partially-built reactors will proceed, and South Korea will still bid for reactor projects overseas).

- Taiwan’s Cabinet reiterated the government’s resolve to phase out nuclear power by 2025 though a long battle

- Japan’s nuclear industry has been decimated ‒ just five reactors are operating (less than one-tenth of the pre-Fukushima fleet) and 14 reactors have been permanently shut-down since the Fukushima disaster (including the six Fukushima Daiichi reactors).

- India’s nuclear industry keeps promising the world and delivering very little ‒ nuclear capacity is just 6.2 GW. In May 2017, India’s Cabinet approved a plan to build 10 indigenous pressurised heavy water reactors, but most have been in the pipeline for years and it’s anyone’s guess how many (if any) will actually be built.

- The UK’s nuclear power program faces “something of a crisis” according to an industry lobbyist. The reactor fleet is ageing but only two new reactors are under construction. The estimated cost of the two Hinkley Point reactors, including finance, is A$40 billion.

- All of Germany’s reactors will be closed by the end of 2022 and all of Belgium’s will be closed by the end of 2025.

- Russia’s Rosatom began construction of the first nuclear power reactor in Bangladesh, signed agreements to build Egypt’s first power reactors, and is set to begin work on Turkey’s first reactors ‒ but Rosatom deputy general director Vyacheslav Pershukov said in June 2017 that the possibilities for building new large reactors abroad are almost exhausted. He said Rosatom expects to be able to find customers for new reactors until 2020‒2025 but “it will be hard to continue.”

- A High Court judgement in South Africa in April 2017 ruled that much of the country’s nuclear new-build program is without legal foundation, and there is little likelihood that the program will be revived given that it is shrouded in corruption scandals and President Jacob Zuma’s hold on power is weakening.

The only nuclear industry that is booming is decommissioning ‒ the World Nuclear Association anticipates US$111 billion worth of decommissioning projects to 2035.

The Era of Nuclear Decommissioning

The ageing of the global reactor fleet isn’t yet a crisis for the industry, but it is heading that way. In many countries with nuclear power, the prospects for new reactors are dim and rear-guard battles are being fought to extend the lifespans of ageing reactors that are approaching or past their design date.

Perhaps the best characterisation of the global nuclear industry is that a new era is approaching ‒ the Era of Nuclear Decommissioning ‒ following on from its growth spurt from the 1960s to the ’90s then 20 years of stagnation.

The Era of Nuclear Decommissioning will entail:

- A slow decline in the number of operating reactors.

- An increasingly unreliable and accident-prone reactor fleet as ageing sets in.

- Countless battles over lifespan extensions for ageing reactors.

- An internationalisation of anti-nuclear opposition as neighbouring countries object to the continued operation of ageing reactors (international opposition to Belgium’s ageing reactors is a case in point ‒ and there are numerous other examples).

- Battles over and problems with decommissioning projects (e.g. the UK government’s £100+ million settlement over a botched decommissioning tendering process).

- Battles over taxpayer bailout proposals for companies and utilities that haven’t set aside adequate funds for decommissioning and nuclear waste management and disposal. (According to Nuclear Energy Insider, European nuclear utilities face “significant and urgent challenges” with over a third of the continent’s nuclear plants to be shut down by 2025, and utilities facing a €118 billion shortfall in decommissioning and waste management funds.)

- Battles over proposals to impose nuclear waste repositories and stores on unwilling or divided communities.

The Era of Nuclear Decommissioning will be characterised by escalating battles (and escalating sticker shock) over lifespan extensions, decommissioning and nuclear waste management. In those circumstances, it will become even more difficult than it currently is for the industry to pursue new reactor projects. A feedback loop could take hold and then the nuclear industry will be well and truly in crisis ‒ if it isn’t already.

News Source: Link